Common Borrower Mistakes When Making Early Loan Repayments

Repaying loans early can seem like an excellent way to reduce debt and save on interest, but without careful planning, early repayments can sometimes lead to unintended consequences. Whether it’s a mortgage, personal loan, car loan, or student loan, borrowers often make mistakes when trying to pay off their loans early. These errors can affect their finances in ways they might not anticipate. In this article, we will explore some of the most common mistakes borrowers make when making early loan repayments and how to avoid them.

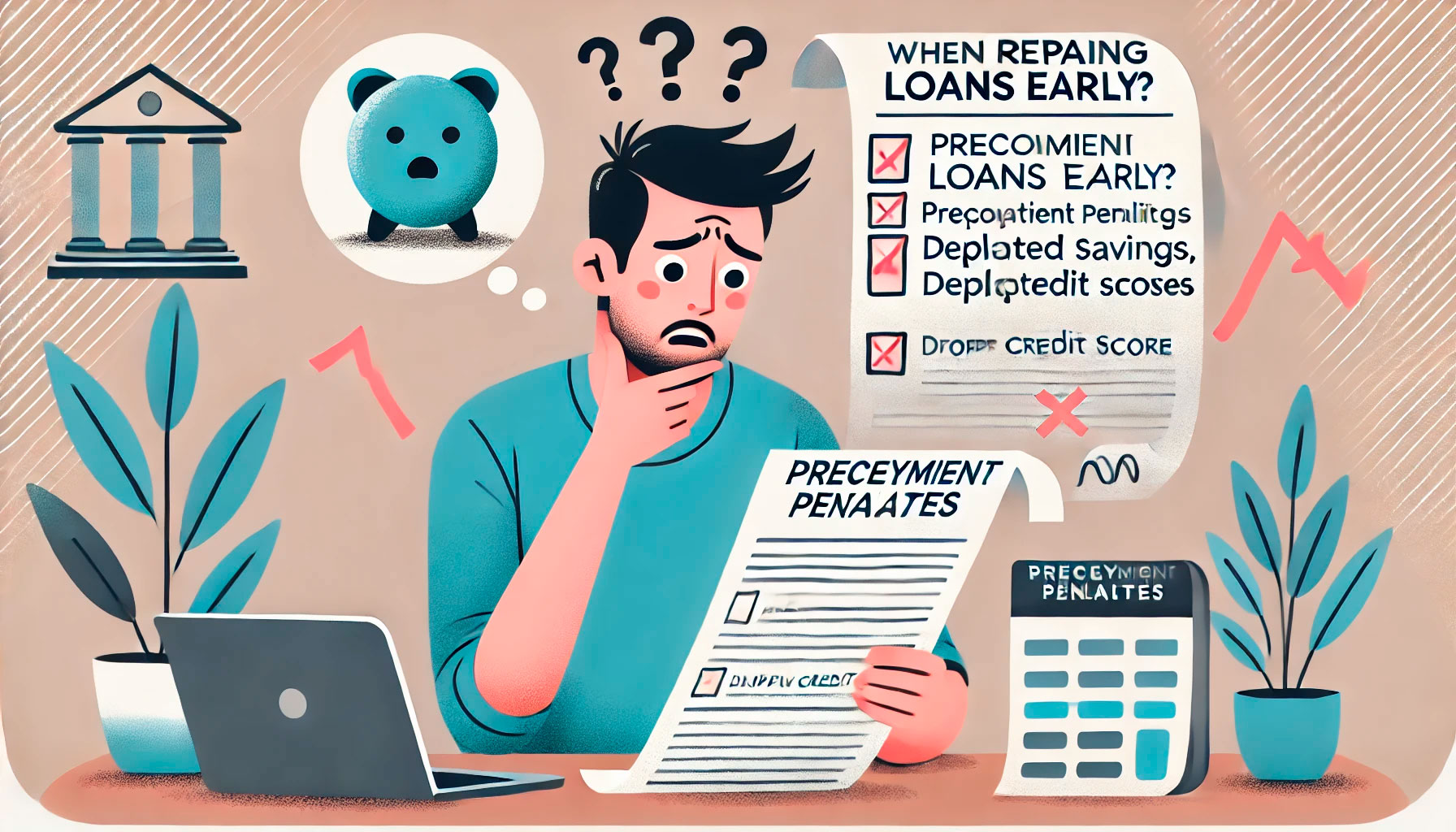

Not Checking Loan Terms for Prepayment Penalties

One of the most common mistakes borrowers make when considering early loan repayments is failing to check the terms of their loan for prepayment penalties. Some loans, particularly mortgages or auto loans, may include clauses that penalize borrowers for paying off the loan early. These penalties can range from a flat fee to a percentage of the remaining loan balance and can significantly reduce the financial benefit of paying off the loan early. To avoid this mistake, borrowers should always review the loan agreement carefully before making additional payments or paying off the loan in full. If prepayment penalties exist, it’s important to calculate whether the savings in interest outweigh the penalty costs.

Focusing Only on Paying Off High-Interest Debt

While it’s understandable to want to pay off high-interest debt first, borrowers may make the mistake of focusing solely on these loans while neglecting other forms of debt that may have more favorable terms. For example, student loans or mortgages may offer lower interest rates or tax benefits that make them less pressing to pay off early. Prioritizing high-interest debt is generally a smart strategy, but it’s important to also consider your financial goals and the terms of all your loans. In some cases, it might make more sense to invest extra funds rather than pay off a low-interest loan early, especially if there are other financial goals, such as building an emergency fund or saving for retirement, that could take precedence.

Not Maintaining an Emergency Fund

One of the biggest risks when making early loan repayments is the potential to deplete an emergency fund. Borrowers may be so eager to pay off their loans early that they neglect to maintain adequate savings for unexpected expenses. It’s essential to remember that life is unpredictable, and having an emergency fund is a crucial financial safety net. Using all your extra funds to pay off loans early could leave you without cash to cover medical expenses, car repairs, or job loss. It’s always wise to keep enough in savings to cover at least three to six months’ worth of living expenses before making large early loan repayments.

Not Considering the Impact on Credit Score

Another common mistake borrowers make when repaying loans early is not understanding how their actions affect their credit score. While paying off debt early can improve your credit utilization ratio, it’s important to note that closing accounts too quickly or paying off loans before the original term can sometimes have negative effects. For example, if you pay off a credit card in full and then close the account, it could reduce your overall available credit and increase your credit utilization ratio, which might hurt your score. Similarly, repaying a loan early can reduce the diversity of your credit mix, which is another factor that affects your score. It’s important to carefully consider the impact of paying off loans on your credit score and to avoid making decisions that could lower it in the long run.

Assuming Paying Off the Loan Faster Saves the Most Money

Many borrowers assume that paying off their loans faster always leads to the most savings. While this is generally true in terms of reducing the total interest paid over the life of the loan, it’s important to understand the specific terms of your loan before accelerating payments. For example, some loans may have fixed interest rates and early repayment won’t save as much as you expect. In contrast, loans with variable interest rates may save more by being paid off early, as the rate could increase over time. Understanding how your interest is calculated and whether additional payments will reduce the principal or just cover interest is essential in determining how much you will actually save. Sometimes, restructuring the loan for a lower interest rate or refinancing might provide better savings than simply making early repayments.

Forgetting to Reevaluate Financial Goals

When borrowers become focused on paying off loans early, they often lose sight of their broader financial goals. Paying down debt is important, but it shouldn’t come at the expense of other essential objectives, such as saving for retirement, contributing to a college fund, or purchasing a home. It’s easy to get caught up in the desire to be debt-free, but it’s crucial to balance loan repayment with other savings goals. Reassessing your financial priorities periodically can help ensure that you don’t sacrifice long-term financial stability for the sake of paying off loans early. In some cases, allocating funds toward investments might yield better long-term returns than paying off debt sooner than necessary.

Missing the Opportunity for Tax Deductions

Some loans, particularly mortgages and student loans, offer tax deductions for the interest paid. For example, mortgage interest payments may be deductible on your tax return, reducing your overall tax liability. When borrowers pay off these loans early, they may inadvertently lose out on these valuable deductions. While paying off debt early is generally beneficial, it’s important to weigh the impact on your tax situation. In some cases, it may make more sense to continue making regular payments to take advantage of the tax benefits, rather than using those funds to pay off the loan faster.

Making early loan repayments can be a great way to reduce debt, save on interest, and improve your financial position. However, borrowers often make mistakes that can negate these benefits. By avoiding common errors like neglecting prepayment penalties, failing to maintain an emergency fund, and not considering the impact on credit scores, borrowers can make more informed decisions when repaying their loans. It’s crucial to carefully evaluate your loan terms, consider all your financial goals, and consult with a financial advisor if necessary to ensure that early repayments align with your long-term financial strategy. With careful planning and consideration, early loan repayments can be an effective tool for improving your financial health.